Q1 2019 Office Market Insight Report

Office Markets Trends

- As landlords look to compete with the popularity of co-working spaces, speculation suites are increasing in popularity and becoming evermore common across the metro. These suites offer move move-in ready spaces that

allow tenants to limit build-out costs and furniture costs and provides more flexible lease terms. Occupiers also find the search-to-lease process is much faster. - The open office concept craze, popularized by Google and Facebook may be coming to an end. Companies are moving to more functional work spaces that offer a wide range of ways to work. This diverse work environment allows employees to select spaces like huddle rooms, workstations, private offices, and conference rooms that best align with their tasks for the day.

- Construction costs remain high and furniture lead time increases due high demand and low supply. Metal tariffs have also played a role in the cost of materials and their availability.

- As parking lots and ramps are redeveloped into commercial spaces, parking in urban areas like Minneapolis is becoming increasingly sparse and more expensive.

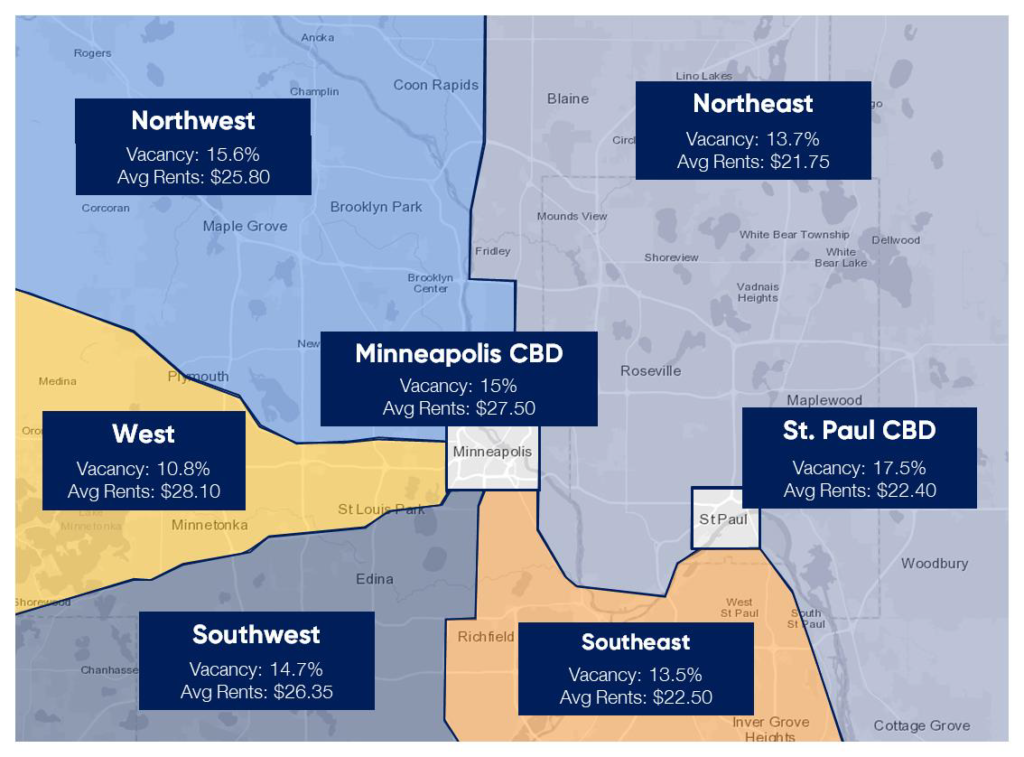

Rental and Vacancy Rates

(click to enlarge)

Market Movement

| Company | Trans. Type | Size | Submarket | Building |

|---|---|---|---|---|

| WeWork | New Location | 102,000 SF | Southwest | Mozaic East |

| Alula | Relocation | 68,000 SF | Northeast | Midway Innovation Ctr |

| Digi International | Relocation | 72,000 SF | West | Excelsior Crossings |

| Tactile Medical | Relocation | 100,000 SF | West | 3701 Wayzata |

| Common Ground | New Location | 25,500 SF | Minneapolis | 801 Marquette |

Investment Sales

| Building | Size | Buyer | Submarket | Price |

|---|---|---|---|---|

| Target Plaza | 310,000 SF | Menlo Equities | Minneapolis | $171M |

| SPS Tower | 620,000 SF | Sumitomo Corp. | Minneapolis | $144M |

| Excelsior Crossings | 268,000 SF | Acesso Partners | West | $115.5M |

| 180 East 5th | 672,000 SF | Gamma Real Estate | St Paul | $52M |

| Minnesota Center | 277,044 SF | Altus | Southwest | $48.6M |

| 3701 Wayzata | 310,000 SF | Opus | West | $22.1M |

The Minneapolis/St. Paul Office Market is a diverse, stable market with an unemployment rate of 2.2% and projected GDP growth that is expected to continue to outperform the national economy. Minneapolis/St. Paul, collectively referred to as the Twin Cities, is the 16th largest MSA with approximately 3.6 million residents and home to 19 Fortune 500 public companies’ headquarters. The Twin Cities is also ranked highly for quality of life, labor force participation, health care and workforce quality.